The Conviction

Datadog is a buy at $114.

The stock has been cut nearly in half from its November 2025 all-time high of $202, swept up in the "SaaS Apocalypse" trade that assumes AI will automate away software companies. For most SaaS businesses, that fear deserves serious scrutiny. For Datadog, it gets the causality exactly backwards. Every new AI model deployed into production needs monitoring for latency, hallucination rates, token costs, and drift. Every autonomous agent framework creates distributed systems with failure modes that no human can trace manually. Every RAG pipeline adds retrieval, embedding, and inference steps that all generate telemetry. AI does not shrink the observability market. It is the single largest expansion of it in a decade.

The Q4 FY2025 numbers confirm this is not just theory. Revenue hit $953 million, up 29% year over year, the fastest quarterly growth rate since Q1 2024 (Datadog Q4 FY2025 Earnings Release, February 10, 2026). Full-year revenue reached $3.43 billion, up 28%. Bookings surged to a record $1.63 billion, up 37%, including two deals exceeding $100 million in total contract value. Remaining performance obligations jumped 52% to $3.46 billion. Free cash flow was $915 million at a 27% margin. The balance sheet holds $4.47 billion in cash against $1.74 billion in convertible notes, yielding net cash of $2.73 billion.

At roughly 10x next-twelve-month revenue and 55x NTM non-GAAP EPS, this is the cheapest Datadog has traded since the 2022 SaaS drawdown. The sell-side agrees: 33 to 43 analysts carry a consensus Buy with an average target near $177 (MarketBeat, March 2026). The base case DCF implies a price above $135. The bull case, driven by AI re-acceleration and a 13x exit multiple, implies $185.

| Metric | FY2023 | FY2024 | FY2025 | FY2026E |

|---|---|---|---|---|

| Revenue | $1.68B | $2.68B | $3.43B | $4.06-4.10B |

| YoY Growth | 27% | 60% | 28% | 18-20% |

| Non-GAAP Op Income | $416M | $673M | $768M | $840-880M |

| Free Cash Flow | $525M | $775M | $915M | ~$1B+ |

| FCF Margin | 31% | 29% | 27% | ~25% |

| Net Revenue Retention | ~115% | ~118% | ~120% | ~120% |

| Customers | ~27,300 | ~29,800 | ~32,700 | ~35,000+ |

The Business

Datadog is the largest independent cloud observability platform. It ingests trillions of events daily from customer infrastructure, applications, and security environments, then converts that data into dashboards, alerts, and automated responses. If something breaks at 2 a.m. in your Kubernetes cluster, Datadog is how the on-call engineer finds out and fixes it before customers notice.

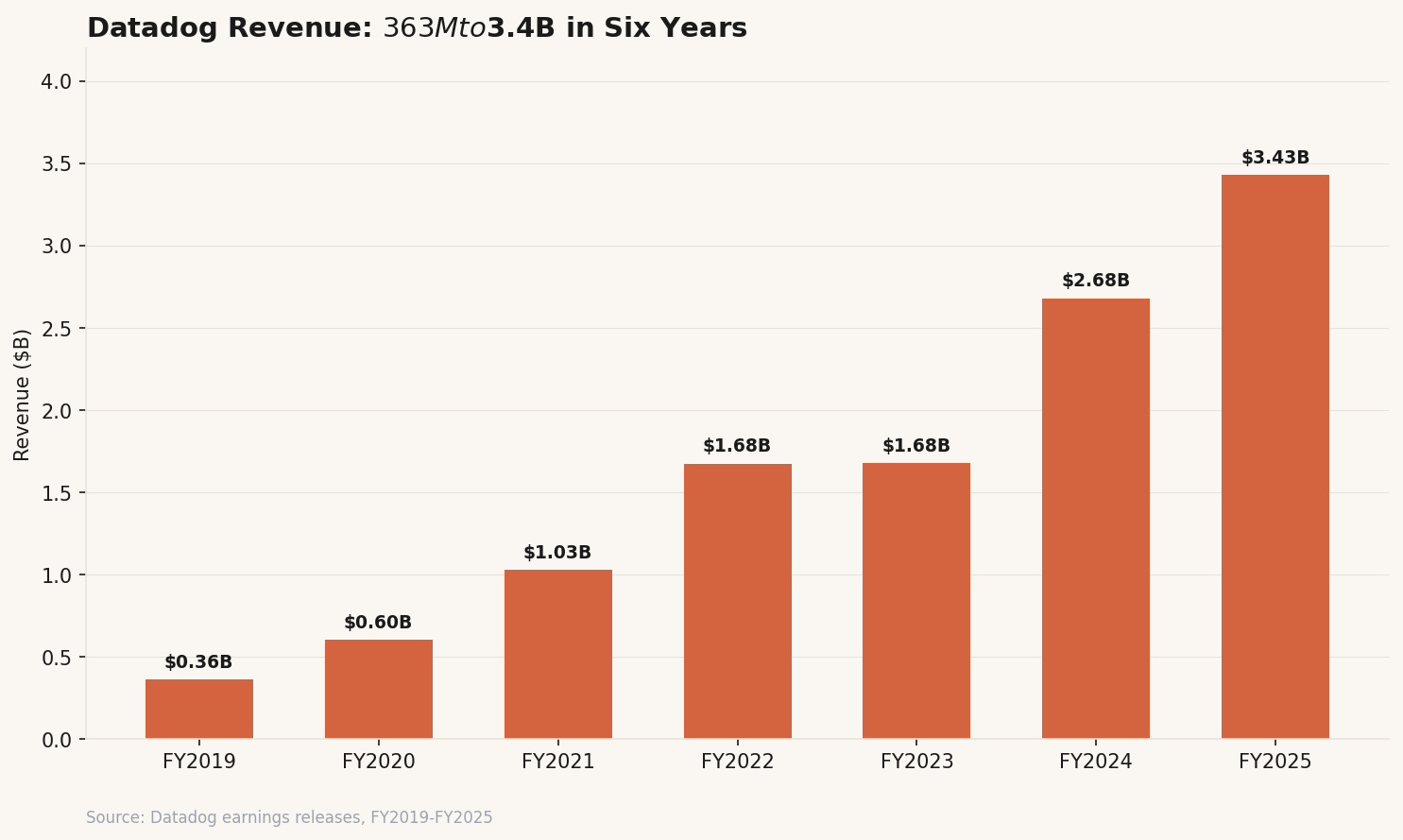

Founded in 2010 by Olivier Pomel and Alexis Le-Quoc, both former engineers at Wireless Generation, the company went public in September 2019 at $27 per share. Revenue has compounded at roughly 45% annually since then, from $363 million in FY2019 to $3.43 billion in FY2025 (Datadog FY2019-FY2025 earnings releases). The platform now spans 26+ products across infrastructure monitoring, APM, log management, cloud security (SIEM, CSPM, application security), digital experience monitoring, CI/CD visibility, and the newest additions: LLM Observability, AI Security, and an autonomous AI SRE agent called Bits AI.

The business model is consumption-based. Customers pay for the volume of telemetry they send through the platform. This creates direct correlation with cloud infrastructure spend: as enterprises run more workloads, they generate more data, and Datadog's revenue grows. The 2023 "cloud optimization" episode revealed the risk in this model (growth dipped when customers cut cloud budgets), but it also means Datadog participates dollar-for-dollar in every new workload deployed.

The Case

Three drivers determine whether Datadog re-rates from here: AI as a demand accelerator, platform consolidation deepening wallet share, and a bookings-to-revenue conversion pipeline that the FY2026 guide materially understates.

Driver 1: AI Creates More Infrastructure to Monitor, Not Less

The bear thesis on SaaS assumes AI replaces software workflows. For observability, the math runs the other direction. A single LLM inference call can touch a load balancer, an API gateway, a model router, a GPU cluster, a vector database, and a caching layer. Each of those components generates telemetry. Multiply that by thousands of concurrent requests and you begin to understand why Datadog's AI-native customer cohort is its fastest-growing segment.

The numbers are concrete. As of Q4 FY2025, approximately 650 AI-native customers use Datadog, including 14 of the top 20 AI-native companies, with 19 spending $1 million or more annually (Datadog Q4 Earnings Call, February 10, 2026). More than 5,500 customers have activated Datadog's AI integrations. The number of MCP server tool calls rose 11-fold quarter over quarter in Q4. And the non-AI base is accelerating too: revenue growth from the broad customer base excluding AI-native customers hit 23% year over year in Q4, up from 20% in Q3.

“We are even more excited about 2026 as we are starting to see an inflection in AI usage by our customers into the application, and as our customers begin to adopt AI innovation, such as the AI SRE agent.”

Olivier Pomel, Chief Executive Officer — Q4 FY2025 Earnings Call, February 10, 2026

On the product side, Datadog is not just watching AI happen to its customers. It shipped LLM Observability, AI Security, and the Bits AI SRE Agent (an autonomous system that investigates alerts, correlates telemetry across services, and surfaces root causes) in the second half of FY2025. Bits AI already has over 2,000 trial and paying customers running investigations within a month of general availability. More than 1,000 customers use the AI observability product (Datadog Q4 Earnings Call, February 10, 2026). This shifts Datadog from passive monitoring tool to active participant in incident resolution, a meaningfully larger addressable market. Management estimates the total addressable market at $65 billion or more when you include adjacent categories like security, service management, and developer tools (Datadog Q4 FY2025 Earnings Release, February 10, 2026).

Driver 2: The Platform Flywheel Has Not Peaked

Datadog's land-and-expand model is among the most effective in enterprise software. Net revenue retention sits at approximately 120%, meaning the average customer spends 20% more each year before any new logo contribution. Gross retention is in the mid-to-high 90s (Datadog Q4 FY2025 Earnings Release, February 10, 2026). These are best-in-class numbers for a consumption model.

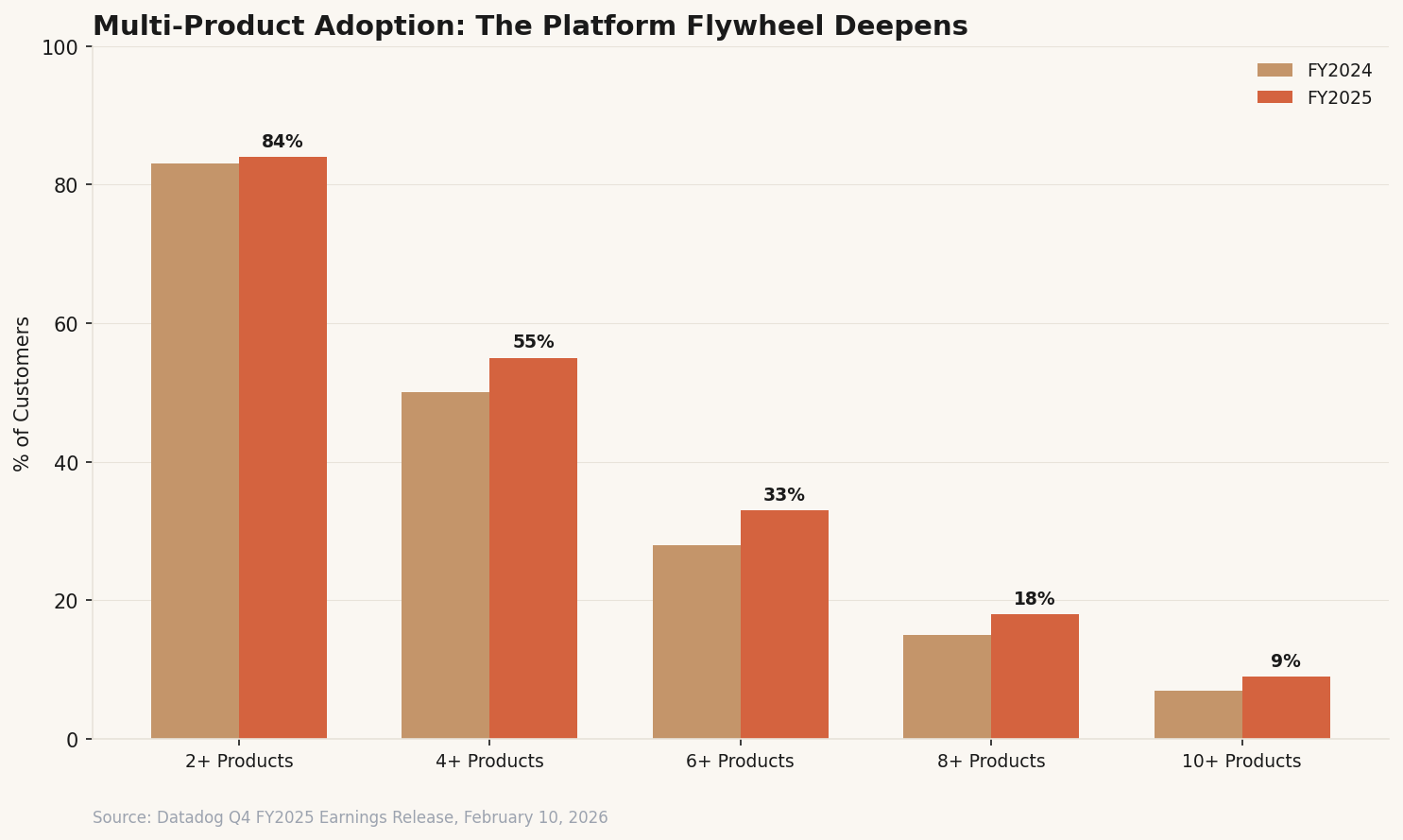

The multi-product adoption data tells the deeper story. At the end of Q4 FY2025, 84% of customers used two or more products (up from 83% a year ago), 55% used four or more (up from 50%), 33% used six or more (up from 28%), 18% used eight or more (up from 15%), and 9% used ten or more (up from 7%). Every single tier increased year over year (Datadog Q4 FY2025 Earnings Release, February 10, 2026). The steepest acceleration is in the deeper tiers, which signals that customers who already trust the platform are adopting new products faster than new customers are landing.

“About half of our customers do not buy all three pillars from us, or at least not yet.”

Olivier Pomel, Chief Executive Officer — Q4 FY2025 Earnings Call, February 10, 2026

That quote should stop you. Half of Datadog's 32,700 customers have not yet adopted all three core observability pillars (infrastructure, APM, and logs). The expansion runway within the existing install base is enormous. Fortune 500 penetration reached 48%, with median ARR per Fortune 500 customer still under $500,000 (Datadog Q4 FY2025 Earnings Release, February 10, 2026). That ceiling has room to rise, especially as the enterprise sales force grew from roughly 450 to 600 reps during FY2025.

Each of the three foundational product pillars crossed major ARR milestones in FY2025: infrastructure monitoring exceeded $1.6 billion, log management surpassed $1 billion (with FlexLogs, the cost-optimized tier, nearing $100 million), and APM hit $750 million and is accelerating. The quarter included 18 deals over $10 million in TCV and two over $100 million. Pomel noted on the call that the company landed an 8-figure annual deal with one of the largest AI financial model companies, its biggest new logo to date (Datadog Q4 Earnings Call, February 10, 2026).

Driver 3: Bookings Tell You What Revenue Won't (Yet)

Here is the number the market is mispricing: $1.63 billion in Q4 bookings, up 37% year over year, against $953 million in Q4 revenue, up 29%. Bookings are growing 800 basis points faster than revenue. That gap represents contracted future revenue that has not yet flowed through the income statement.

Remaining performance obligations of $3.46 billion (up 52%) confirm the backlog accumulating beneath the surface. This is more than a full year of revenue sitting in the pipeline. Management has a documented pattern of conservative guidance. The FY2025 initial guide called for mid-20s growth; actual came in at 28%. The FY2026 guide of $4.06 to $4.10 billion (18-20% growth) explicitly bakes in a cautious assumption for the largest customer.

“Our business, excluding our largest customer, grows at least 20% during the year.”

David Obstler, Chief Financial Officer — Q4 FY2025 Earnings Call, February 10, 2026

The largest customer is widely understood to be an AI-native hyperscaler. Modeling it conservatively is prudent risk management by the CFO, not a growth warning. If AI infrastructure buildout continues at anything close to its current pace, Datadog is more likely to print 22-25% revenue growth in FY2026 than 18-20%. The Q1 FY2026 guide of $951 to $961 million (25-26% growth) already suggests the full-year guide has room to move up.

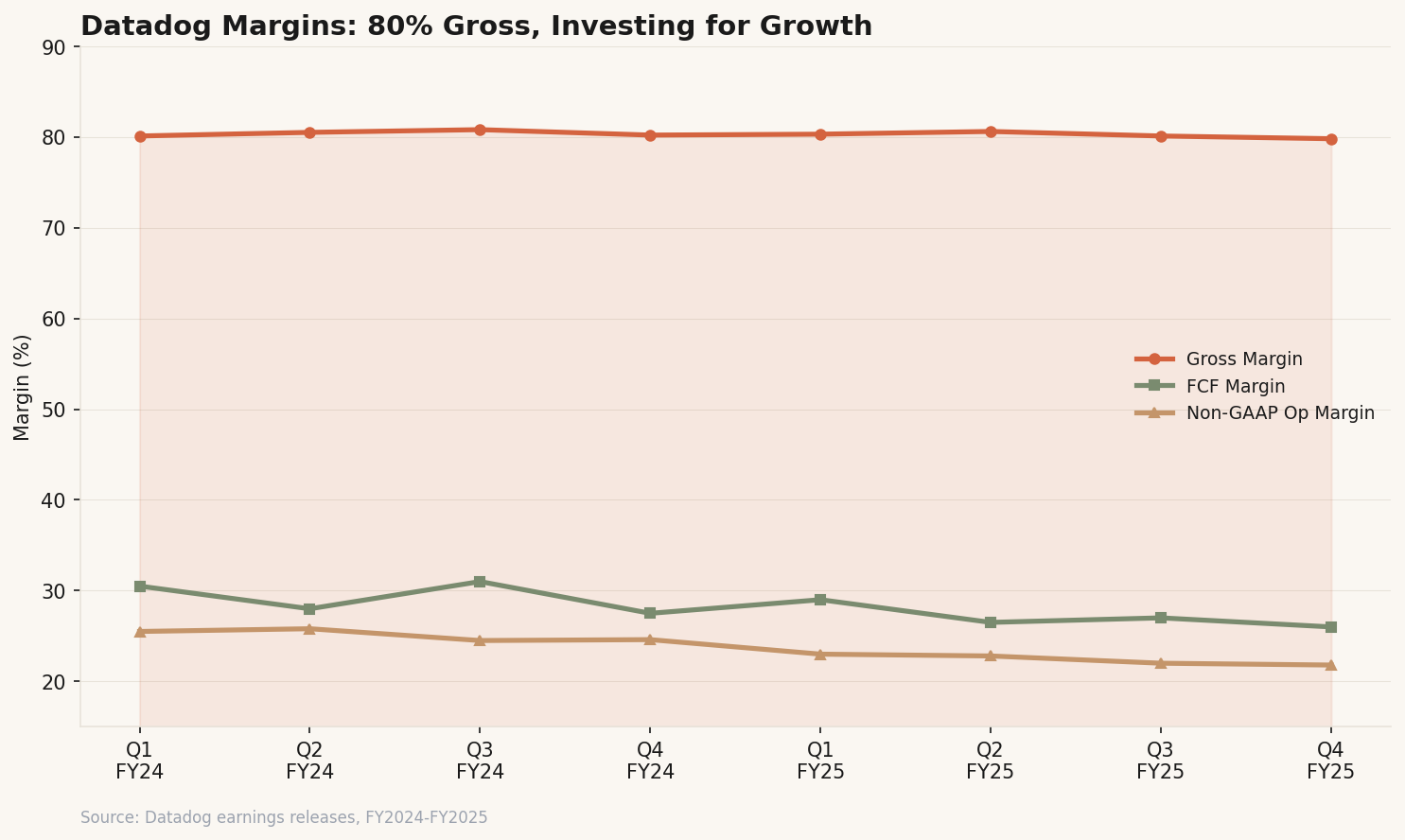

Gross margins remain durable at approximately 80%, funding aggressive R&D investment (400+ new features shipped in FY2025) while generating $915 million in free cash flow. Non-GAAP operating margin of 22.4% dipped from 25.1% in FY2024, a deliberate decision to invest in the enterprise go-to-market motion and new product categories like security and AI observability (Datadog Q4 FY2025 Earnings Release, February 10, 2026). This is a company choosing to invest at the point of maximum opportunity, not one losing operating discipline.

AI re-acceleration drives 22%+ revenue CAGR through FY2030. Platform consolidation deepens. 13x exit multiple on FY2030 revenue.

Growth moderates to high teens. Margins expand as sales force reaches full productivity. 10x exit multiple.

Open-source pricing pressure compresses growth to mid-teens. Cloud optimization cycle repeats. 7x exit multiple.

The Risks

The bull case requires sustained 20%+ growth, and five specific risks could break it.

The competitive field is real but manageable. Dynatrace ($12B market cap, $1.9B ARR, 16-18% growth) competes for enterprise consolidation budgets but grows slower and has a narrower platform. Cisco's $28 billion Splunk acquisition brings bundling distribution but has been slow on the cloud-native transition. Hyperscaler-native tools (AWS CloudWatch, Azure Monitor, Google Cloud Operations) are bundled free but lack multi-cloud depth. The moat has four layers: platform breadth (26+ products), data network effects (trillions of events improving Bits AI and Watchdog anomaly detection), switching costs (mid-to-high-90s gross retention from deep SOC and DevOps workflow integration), and innovation velocity (400+ features shipped in a single year).

| WACC \ Exit | 7.0x | 10.0x | 13.0x |

|---|---|---|---|

| 9.0% | $105 | $155 | $205 |

| 10.0% | $92 | $140 | $185 |

| 10.9% | $80 | $125 | $165 |

| 12.0% | $65 | $100 | $135 |

The Bottom Line

Datadog is the best-positioned company in cloud observability, trading at its lowest valuation multiple in four years while its backlog grows 52% and its AI-native customer cohort expands faster than the core business. The market is treating it like a company whose growth is about to stall permanently. The $1.63 billion in bookings, the $3.46 billion in RPO, and the 650 AI-native customers say otherwise.

The base case is $135. The bull case is $185. The core risk is not competitive (the moat across platform breadth, data network effects, and switching costs is strong) but valuation-related: the market may continue compressing SaaS multiples regardless of fundamentals. The specific things to watch are Q1 FY2026 revenue growth versus the 18-20% full-year guide (a beat toward 22%+ would confirm re-acceleration), AI-native customer count trajectory through the May earnings report, and any signal from the June DASH conference on Bits AI's commercial traction. If Datadog can demonstrate that AI workloads are a durable, multi-year growth driver and not a one-quarter blip, the current price will look cheap in hindsight.