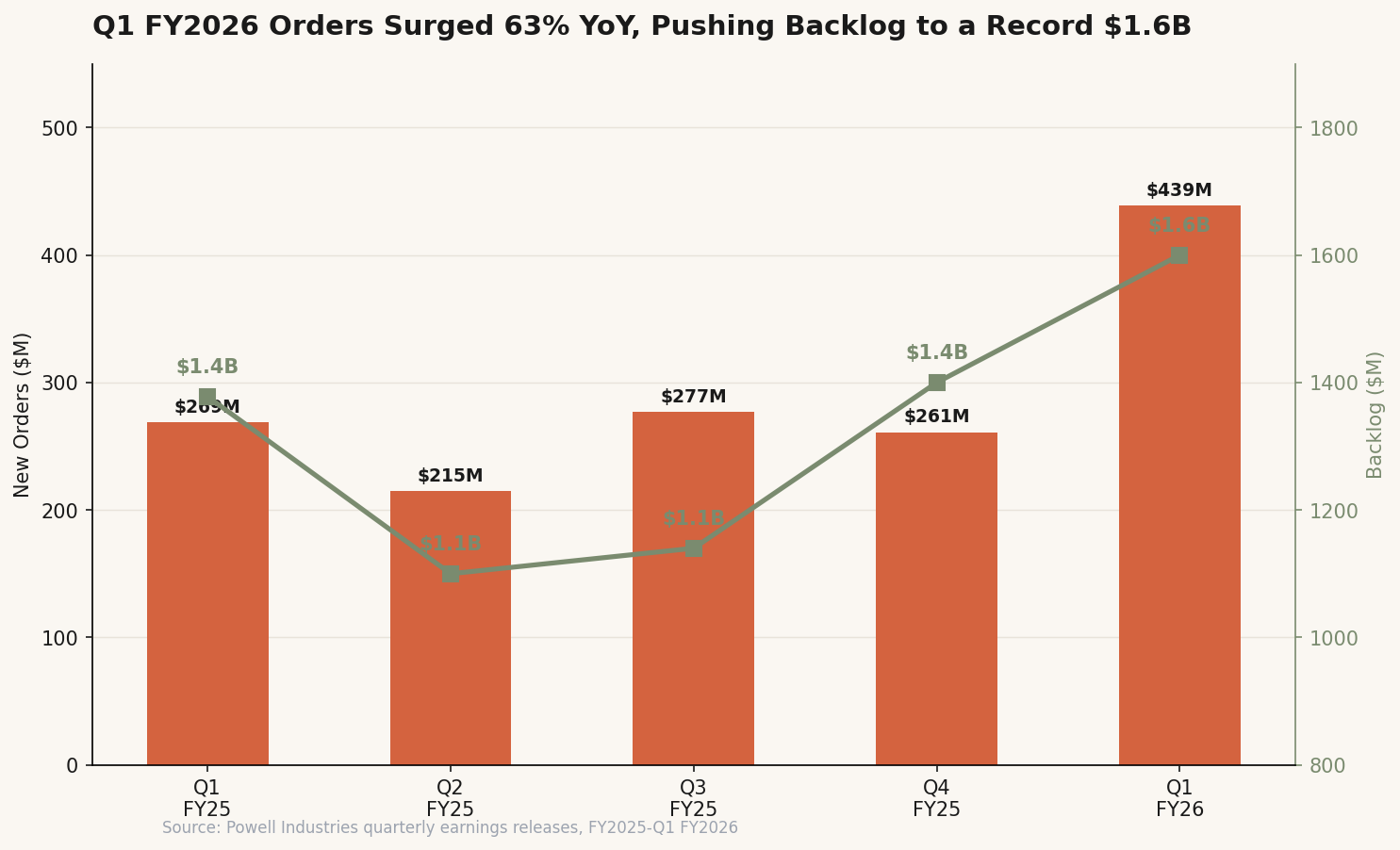

Powell Industries booked $439 million in new orders last quarter. That is a 63% year-over-year increase, the highest quarterly total in over two years, and it included two projects that would have been unthinkable for this company five years ago: a roughly $75 million data center megaproject (Powell's first) and a single domestic LNG terminal award worth more than $100 million (Powell Industries Q1 FY2026 Earnings Release, February 3, 2026). The backlog hit $1.6 billion. The book-to-bill ratio was 1.7x.

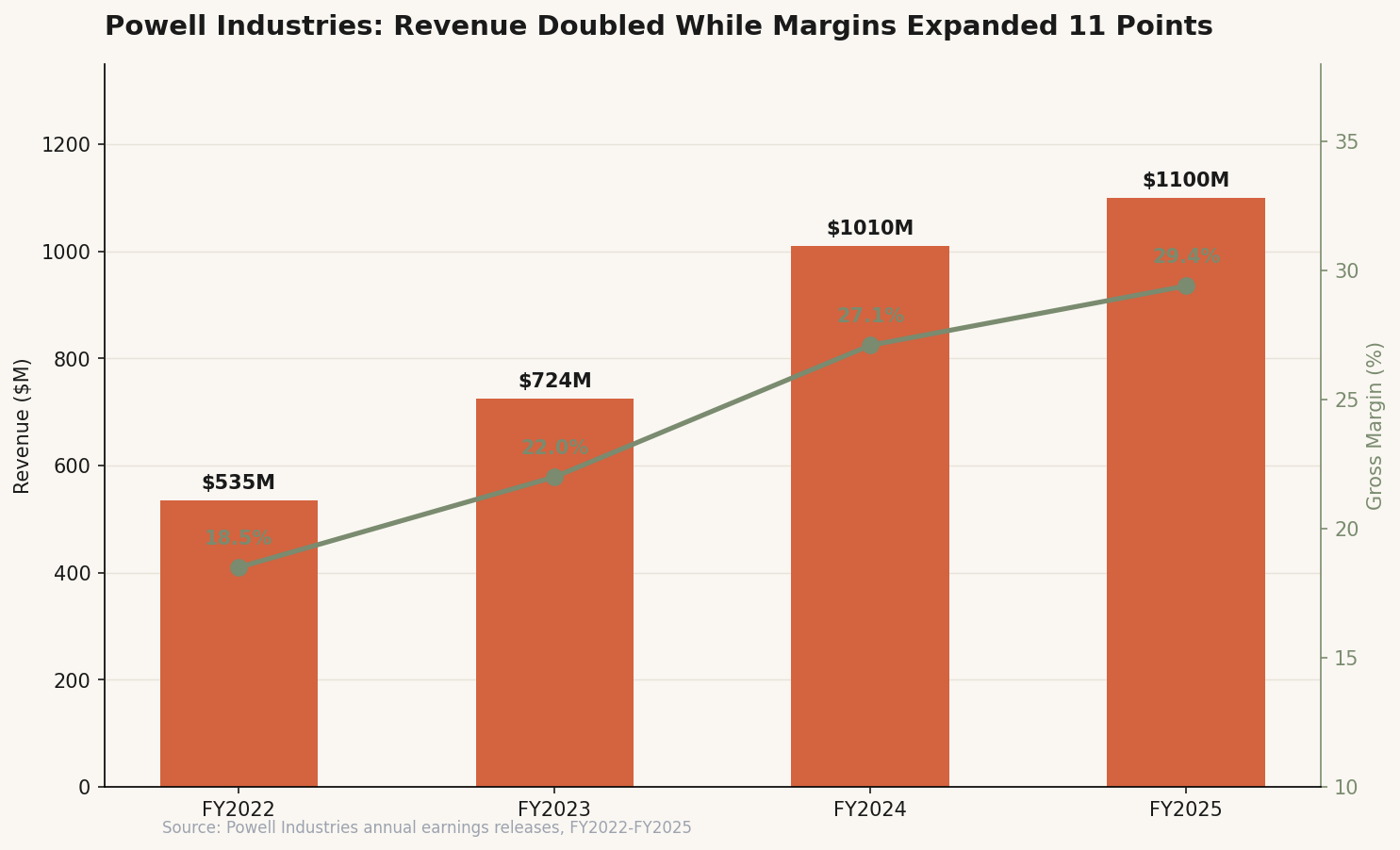

I am bullish on Powell Industries. The valuation at 34x trailing earnings is steep for an industrial company, and I will spend time on why that price tag carries real risk. But the combination of a record backlog with 12 to 18 months of visibility, zero debt, $501 million in cash, and positioning at the exact intersection of grid modernization, LNG exports, and AI-driven power demand makes Powell one of the best risk-reward setups in the electrification trade today. Three years ago, this was a cyclical oil-field equipment supplier trading at 8 to 12x earnings. Revenue was $535 million. Gross margins sat at 18.5%. Today, revenue has doubled to $1.1 billion, gross margins have expanded to 29.4%, and the stock is up roughly 270% over the past two years (Powell Industries FY2025 Earnings Release, November 19, 2025).

The thesis is not complicated. It is about three spending cycles converging on a single company at the same time. What makes it interesting is that Powell did not stumble into this position. CEO Brett Cope has spent nearly a decade repositioning the company away from pure oil-and-gas dependence. The Q1 FY2026 results are the first quarter where all three end markets (data centers, LNG, utilities) showed up in the order book simultaneously.

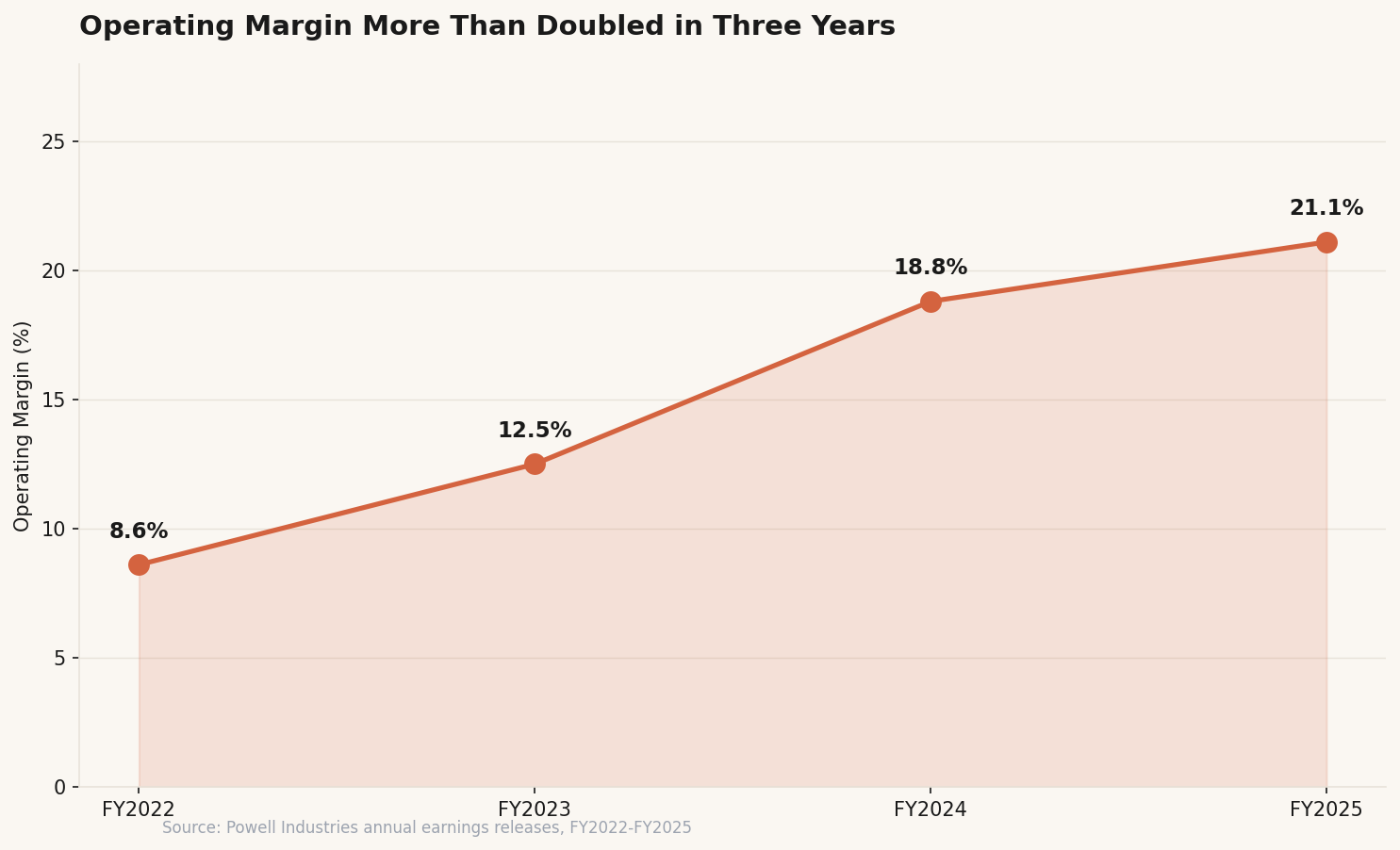

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Revenue | $535M | $724M | $1,010M | $1,100M |

| Gross Margin | 18.5% | 22.0% | 27.1% | 29.4% |

| Operating Margin | 8.6% | 12.5% | 18.8% | 21.1% |

| Net Income | $27M | $62M | $149M | $181M |

| Diluted EPS | $2.25 | $5.15 | $12.31 | $14.86 |

| Backlog | $590M | $822M | $1,100M | $1,400M |

The Business

Powell Industries, founded in 1947 and headquartered in Houston, designs and manufactures custom-engineered electrical equipment for distributing, controlling, and monitoring electrical energy. The product line includes integrated power control rooms, electrical houses (E-houses), arc-resistant switchgear, and medium-voltage circuit breakers. None of these are catalog items. Each system is engineered to a specific customer's specifications, with lead times of 12 to 24 months.

The customer base spans oil and gas, LNG terminals, petrochemical plants, electric utilities, data centers, and mining operations. The key metric for this business is backlog, because it tells you what revenue will look like 12 to 18 months from now. At $1.6 billion as of December 2025, with $933 million expected to convert in the next twelve months, the revenue line has a degree of visibility that most industrial companies would envy (Powell Industries Q1 FY2026 10-Q).

The business is capital-light by industrial standards. CapEx runs at just 1.5 to 2.0% of revenue (Powell Industries FY2025 10-K). That means margin expansion drops through to cash flow almost dollar-for-dollar. Powell generated approximately $170 million in free cash flow in FY2025 on $1.1 billion in revenue, a 15.5% FCF margin. For an industrial manufacturer, those are exceptional economics.

The Case

Three overlapping infrastructure spending cycles are driving Powell's transformation from a cyclical oil-field supplier into something that looks much more like a secular growth story. Each one is a multi-year, multi-billion-dollar theme. The unusual part is that all three are hitting at the same time.

Data Centers: The Newest and Fastest-Growing End Market

Two years ago, data centers were not a meaningful part of Powell's business. In Q1 FY2026, total data center orders exceeded $100 million in a single quarter (Powell Industries Q1 FY2026 Earnings Release, February 3, 2026). The roughly $75 million megaproject booking was the company's first in this end market, and management framed it as the beginning of something bigger.

“The rapid pace of data center development and AI investment is leading to larger and more numerous opportunities for Powell in our Commercial and Other Industrial market, demonstrated by the growing market opportunity for our medium-voltage switchgear product to handle the power demands of larger data centers with greater computing power.”

Brett Cope, Chairman and CEO, Powell Industries — Q1 FY2026 Earnings Call, February 4, 2026

The logic is straightforward. Large-scale AI training clusters require hundreds of megawatts per facility. That power needs to be distributed, controlled, and monitored through medium-voltage switchgear and E-houses. Those are exactly the products Powell has been building for oil refineries and LNG terminals for decades. The engineering complexity is comparable. The dollar values per project are comparable. And there is something else: on the Q1 call, Cope described the data center opportunity as increasingly "design one, build many," suggesting that what starts as custom engineering could evolve into more repeatable, production-line work (Q1 FY2026 Earnings Call, February 4, 2026). If that pattern holds, it would be a margin tailwind on top of volume growth.

Powell is adding a 50,000 square foot leased facility specifically to support data center product flow and evaluating additional capacity investments (Q1 FY2026 Earnings Call, February 4, 2026). The company is putting real capital behind this end market, not just talking about it.

LNG: Big Contracts Coming Back

The U.S. is now the world's largest LNG exporter, and Gulf Coast terminal construction is reaccelerating after a period of subdued activity through much of 2024 and early 2025. Powell sits in Houston, adjacent to these projects, and builds the electrical distribution systems that power gas liquefaction and export infrastructure. In Q1 FY2026, a single domestic LNG project valued at more than $100 million landed in the order book (Powell Industries Q1 FY2026 Earnings Release, February 3, 2026).

LNG terminal projects are long-duration, high-complexity, and play directly to Powell's engineering capabilities. The contract values are large. The margins are favorable because of the custom engineering required. And the pipeline of announced-but-not-yet-ordered terminal projects remains substantial. Management noted that "the favorable economics of the U.S. natural gas market will continue to drive international demand for domestic LNG exports" and expects "sustained order activity" from this end market (Q1 FY2026 Earnings Call, February 4, 2026).

Grid Modernization: The Steady Drumbeat

Electric utility revenue grew 35% year-over-year in Q1 FY2026 (Powell Industries Q1 FY2026 Earnings Release, February 3, 2026). The drivers here are aging grid infrastructure, renewable energy interconnection requirements, and raw load growth from electrification across transportation and industry. The Inflation Reduction Act and CHIPS Act provide additional tailwinds through tax credits that encourage utility capital spending. Unlike data centers (which could theoretically pause if AI spending slows) or LNG (which is tied to commodity economics), grid modernization spending is driven by regulatory mandates and physical necessity. The grid is old. It needs to be rebuilt. That creates a floor under Powell's order activity.

“The growing and broad investment in power generation and grid modernization to support data center and AI capacity growth, domestic manufacturing, electrification, and the nationally important export of energy resources like LNG are validating our now nearly decade-long strategic effort to transform Powell into a more diversified manufacturer of electrical distribution products and systems.”

Brett Cope, Chairman and CEO, Powell Industries — Q1 FY2026 Earnings Call, February 4, 2026

That quote matters. Cope is not describing a lucky break. He is describing a strategy that has been in motion since roughly 2017, when the company began deliberately diversifying away from its oil-and-gas roots. Electric utility and data center orders now represent a growing share of the backlog, reducing concentration risk in any single end market.

The Margin Story Is Just as Good as the Revenue Story

The financial transformation goes well beyond top-line growth. Gross margin expanded from 18.5% in FY2022 to 29.4% in FY2025, an increase of nearly 11 percentage points in three years (Powell Industries earnings releases, FY2022-FY2025). Operating margin more than doubled from 8.6% to 21.1% over the same period. This is not just volume flowing through a fixed cost base. It reflects a deliberate mix shift toward higher-complexity projects, improved project execution, and genuine pricing power in a supply-constrained market for custom electrical equipment.

The natural question is whether these margins can hold. CFO Mike Metcalf addressed this directly on the Q1 call. Trailing twelve-month gross margins were running at about 30%, with approximately 175 basis points coming from favorable project closeouts. He called a base margin in the "upper 20s" with an additional 150 to 200 basis points from closeouts a "reasonable assumption" (Q1 FY2026 Earnings Call, February 4, 2026). That framing suggests the margin expansion is mostly structural, not a one-time windfall from a few favorable contracts. The underlying base has moved permanently higher.

Balance Sheet and Capital Allocation

Powell carries zero debt. It held $501 million in cash and short-term investments as of December 2025 (Powell Industries Q1 FY2026 10-Q). For a company with a $6.2 billion market cap, that is a meaningful cash position: roughly 8% of the enterprise value sitting in liquid assets with no offsetting obligations.

The company is investing in capacity expansion, but modestly. The $12.4 million expansion announced in FY2025 focuses on data center and utility-grade equipment manufacturing. The August 2025 acquisition of Remsdaq Ltd., a UK-based SCADA remote terminal unit manufacturer, adds electrical automation capabilities and has been described by management as "margin-accretive" (Q1 FY2026 Earnings Call, February 4, 2026). The 3-for-1 stock split effective April 6, 2026 signals management confidence and broadens the retail investor base (Powell Industries 8-K, March 6, 2026).

Data center orders accelerate beyond expectations. LNG pipeline converts fully. Utility spending sustains. Powell expands capacity and maintains pricing power through the cycle.

Current trajectory continues. Backlog converts on schedule with modest margin normalization from FY2025 peaks. Data center becomes a steady 15-20% of orders.

Oil and gas downturn coincides with a data center spending pause. Margin compression from input costs and competition. Multiple contracts to low-20s P/E.

The Risks

The risks are specific and they are real. At 34x trailing earnings, the stock is priced for sustained execution across all three end markets simultaneously. Any stumble gets punished.

Oil and gas still represents approximately 45% of revenue (Powell Industries FY2025 10-K). The diversification story is improving, but it is incomplete. A commodity downturn or capex cycle reversal in the petrochemical sector would hit Powell directly, even as data center and utility orders grow. The stock would not get credit for the secular growth story if the cyclical half of the business is shrinking.

The $12.4 million capacity expansion is modest relative to the scale of demand. If data center orders accelerate faster than Powell can add manufacturing capacity, the company risks losing share to larger competitors. Eaton ($138B market cap) trades at a comparable 35x P/E but with ten times the revenue base and a global manufacturing footprint (StockAnalysis.com, March 2026). Schneider Electric and Siemens are similarly scaled. Powell's advantage is specialization, not size, and specialization only matters if you can deliver on time.

“I think the $1.6 [billion] is very durable. If you look at the timing and our understanding of the project, I feel very good about it.”

Brett Cope, Chairman and CEO, Powell Industries — Q1 FY2026 Earnings Call, February 4, 2026

Cope's confidence in backlog durability is reassuring, but "very durable" is a qualitative judgment. The $1.6 billion backlog implies $933 million of revenue conversion in the next twelve months, with the remainder stretching further out. Large, complex projects spanning 12 to 24 months carry execution risk: delays, cost overruns, and scope changes that compress margins. Steel, aluminum, and copper are key raw materials, and tariff escalation or commodity price spikes would pressure gross margins, only partially offset by contract escalation clauses. The Q1 FY2026 gross margin of 28.4% included 300 basis points of favorable project closeout impact versus the prior year (Q1 FY2026 Earnings Call, February 4, 2026). That kind of tailwind does not repeat every quarter.

The Bottom Line

Powell Industries is the purest play on U.S. electrical infrastructure spending available in public markets. Grid modernization, LNG terminal construction, and data center power demand are three spending cycles that are each individually multi-year in duration and collectively unprecedented in their simultaneous scale. The financial results reflect this: revenue has doubled in three years, operating margins have more than doubled, and the balance sheet carries $501 million in cash with zero debt.

The risk is the price tag. At 34x trailing P/E, this is not a hidden gem. The market has already recognized the Powell story and priced in continued execution. The question is whether the growth justifies the multiple. I think it does, with one critical caveat: Q2 FY2026 order activity needs to confirm that the Q1 surge was not a one-time anomaly driven by two lumpy megaprojects. A sustained book-to-bill above 1.0x and continued data center project wins would validate the thesis. A quarter where orders normalize back to the $270 to $300 million range would raise legitimate questions about whether Q1 was a pull-forward. Watch the May 2026 earnings report. That is the next real data point.

| WACC \ Exit | 14x | 16x | 18x |

|---|---|---|---|

| 9.5% | $620 | $680 | $750 |

| 10.6% | $470 | $520 | $580 |

| 12.0% | $340 | $370 | $400 |